In his first media appearance of the year, President Buhari reiterated his long-held belief that Nigerians must return to farming in order to address economic challenges. As Buhari-like as this statement may be, the sector’s high growth and export potential make it a viable support mechanism for Nigeria’s macroeconomic and non-oil growth. For example, between January and March 2021, Agriculture contributions made up 22.35 per cent of total GDP.

However, limited financing, among other factors, has had a negative impact on the sector’s productivity, so that 70 per cent of Nigerians working in the sector primarily operate at little above subsistence level with no opportunities to scale and limited or zero access to markets and finance.

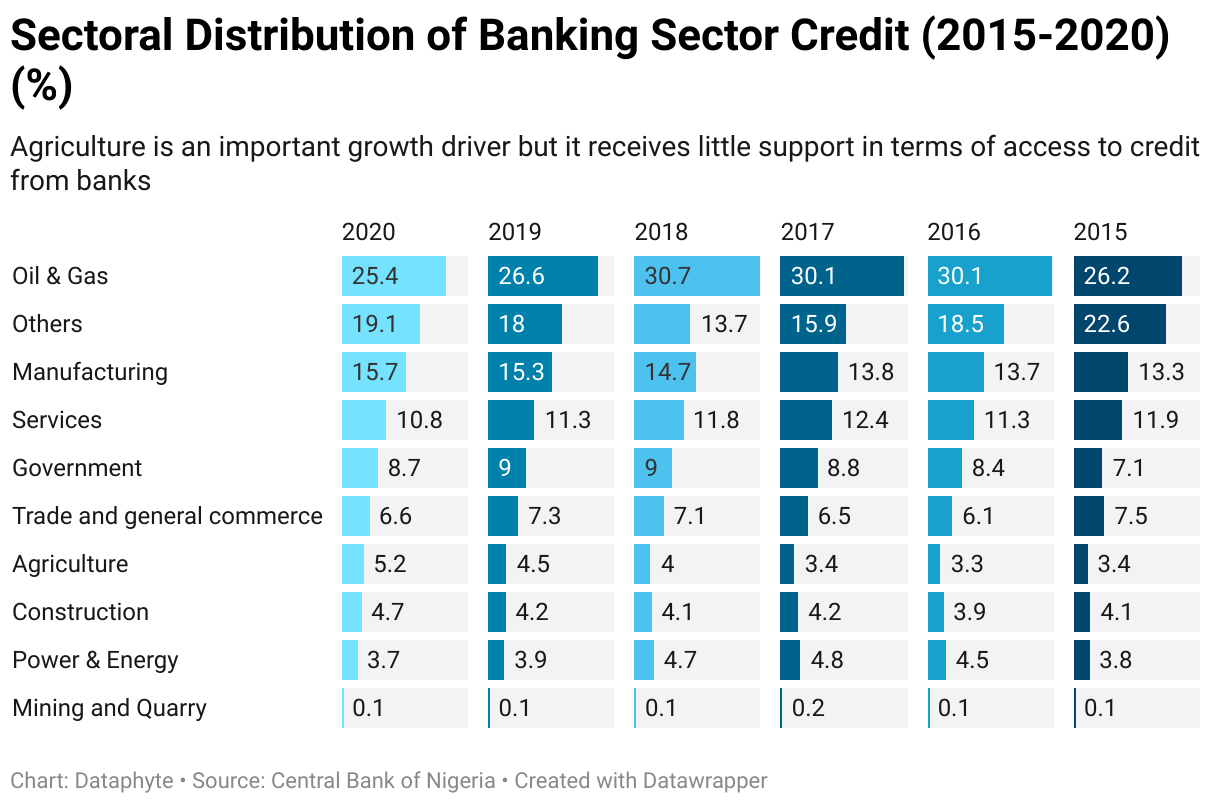

According to Dataphyte’s analysis of the sectoral distribution of banking credit in Nigeria, financial sector institutions lend a disproportionately lower share of their loan portfolios to agriculture when compared to the agriculture sector’s share of GDP. Banks are hesitant to lend to certain sectors, including agriculture, which is one of Nigeria’s most underfunded industries.

While the agricultural sector was responsible for 24.1% of GDP in 2020, credit to the agricultural sector accounted for only 5% of total banking sector credit. This reflects the increased risks associated with lending to agricultural firms that are not part of developed value chains; these businesses account for at least three-quarters of the farming population in the country. The low competitiveness of Nigerian agricultural producers and their produce is also a risk factor.

Low credit to the agricultural sector is consistent over the six-year period under review. The sector, between 2015 and 2018, received the second-lowest banking sector credit only after the mining and quarry sector, which received less than 1% of total banking sector credit. In 2020 and 2019, the agriculture sector received 1.5 and 0.6 per cent more banking sector credit than the power sector. And in the same period under consideration, it received 0.5 and 0.3 per cent more banking credit than the construction sector.

The total value of credit to the sector is nominal in spite of the minor increases recorded in 2019 and 2020.

According to Mr. Adesina, former Agriculture Minister, the agricultural sector has been undercapitalized due to banks’ high demands for collateral, a lack of capacity to develop appropriate credit instruments for agriculture, high perceived risks of lending to this sector, and a general aversion of banks toward agriculture.

In its Anchor Borrowers Programme Guideline, the Central Bank of Nigeria reiterated that, despite the significant level of growth in the Nigerian financial sector, a critical area in which banks continue to seek better results is providing access to financial services and bridging the gap that constrains agricultural sector growth.

In recent years, a major focus of the Central Bank of Nigeria’s directed finance has been to increase funding available to the agriculture sector. The CBN’s development finance and risk-sharing schemes, such as the Anchor Borrowers Program (ABP) launched in 2015 and the Nigeria Incentive-Based Risk Sharing System for Agricultural Lending (NIRSAL), is aimed at increasing agricultural productivity and job creation while catalyzing private bank lending to agriculture.

According to the CBN’s September 2021 report, the CBN has released N798.1 billion to 3.9 million smallholder farmers cultivating 4.9 million hectares of land since the inception of the ABP program.

Despite this, there have been reports of alleged corruption and mismanagement of funds.

A World Bank report suggests that CBN financing to the agriculture sector is weakening and crowding out the financing and loan instruments by commercial banks. The report went on to suggest that future efforts to assess the impact of the CBN’s agricultural financial credit schemes could include highlighting how it avoided the high collateral requirements that deposit money banks typically impose on farmers, as well as guaranteed loan repayments.

Due to a drastic increase in global population and changing dietary preferences of the growing middle class in emerging markets toward higher-value agricultural products, there is an ever-increasing need to invest in agriculture. Furthermore, climate risks heighten the need for investments to make agriculture more resilient to such risks.

If the federal government of Nigeria is serious about agricultural development as a support mechanism for macroeconomic and non-oil growth, innovative, market-based, and commercialized agriculture financial credit schemes that are scalable and reach a large number of beneficiaries should be implemented.

farming farming