The Federal Government (FG) in its May communique of the Federation Account Allocation Committee (FAAC) stated that N97.3 billion was generated from Electronic Money Transfer Levy (EMTL).

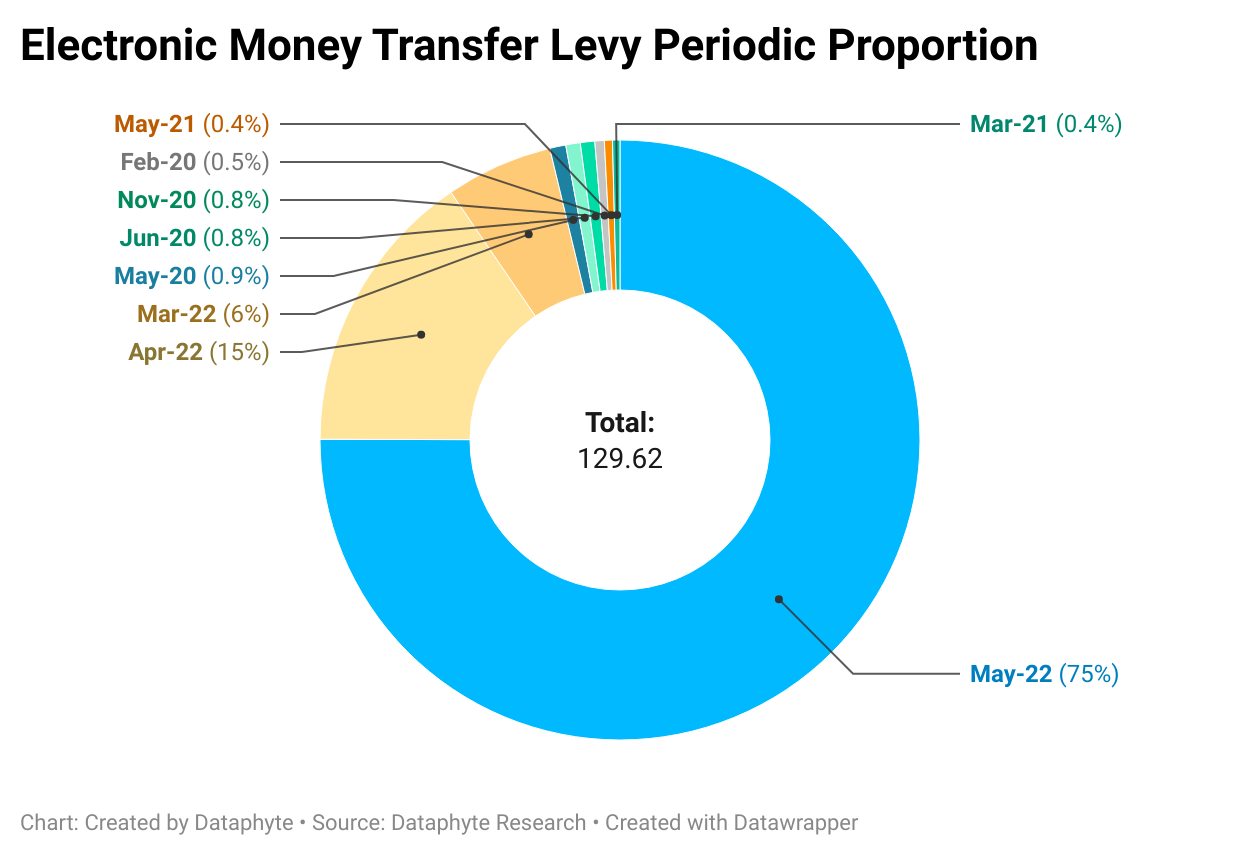

This represents the highest amount generated from EMTL by the country since 2020. Nigeria has generated not less than N129.62 billion from EMTL and the amount generated in April represents 75.04% of the total amount generated thus far.

Revenue generated from EMTL made up 14.29% of the total N680.78 billion generated by the federal government in the month of April.

Electronic money transfer levy was introduced to replace the stamp duty on bank transfers in the 2020 Financial Act. This levy imposes a N50 levy on electronic transfers of money deposited in any financial institution for amounts over N10,000.

What does this mean? It implies that if Sule buys or has a transaction with Chinedu and he pays him using an inter-bank transfer, after crediting the account of Chinedu with the amount, say N10,000, the bank will charge Sule a N50 levy for the transaction, apart from the money transferred. This will mean a total deduction from Sule’s account of N10,050 for the transaction.

This electronic transaction levy appears to apply both ways – from the sender and receiver. So both Sule and Chinedu will receive debit alerts. However, Sule would get an alert of the debit from his bank but Chinedu would not except he pays close attention to his bank statements. Most people don’t.

Chinyere Janice, who sells groceries, noted deductions termed ‘levy’ on her account.

‘For every bank alert I receive as payment for the items I supply, my money is being deducted as an electronic transfer levy. This amount ranges from N10 to N100, depending on the amount transferred to my account,’ Chinyere said.

Electronic money transfer levy is a source of revenue for most African countries. A report termed it ‘lazy tax’ as the government doesn’t have to do much to collect it.

The report shows that Uganda was the first to impose this levy in Africa in July 2018 with a 0.5% threshold. Zimbabwe followed in October 2018 at 2% taxation threshold. For all countries that have imposed this levy, the threshold ranges from 0.2% to 2%.

Nigeria introduced this in the 2020 Financial Act and has since commenced collection. Section 89 (A)(1&2) of the act states:

There is imposed a levy, to be referred to as the Electronic Money Transfer Levy, on electronic receipts or electronic transfer for money deposited in any deposit money bank or financial institution, on any type of account, to be accounted for and expressed to be received by the person to whom the transfer or deposit is made

The levy shall be imposed as a singular and one-off charge of N50 on electronic receipts or electronic transfers of money in the sum of N10,000 or more

Sub-section 2 of the act states a one-off deduction payment.

Nigeria has continued to witness increased adoption of mobile banking for transactions as a critical part of the financial inclusion strategy. Transaction volume through mobile devices between January and April 2022 was 153 million. In 2021 within the same period, transaction volume was 67 million, a 128.4 percent year-on-year increase.

Nigeria, alongside 6 other countries contribute half of the World’s 1.7 billion unbanked population. For financial institutions and the many fintech companies springing up, there is still a substantial market to tap into.

Expanding the mobile banking market is also good news for a revenue-challenged Nigeria because as that market grows, the levy on electronic transfers will provide increased revenue to the government, even if it amounts to double jeopardy for users of mobile banking services, both senders and receivers.

Get real time update about this post categories directly on your device, subscribe now.

{kind=link}