Today, a new generation of Nigerians live through the country’s prolonged battle with two of its biggest socio-economic deficiencies – a protracted housing deficit and recurrent budget deficits.

These two big deficits threaten the fiscal and physical well-being of the government and the people respectively.

China’s recent treatment of Uganda in taking over its vital national asset in lieu of its unpaid debts caused debt-borne disgrace to the country and its nationals. It also portends a bad omen to other African countries who go cap-in-hand to access loans to fund the inept management of their respective economies.

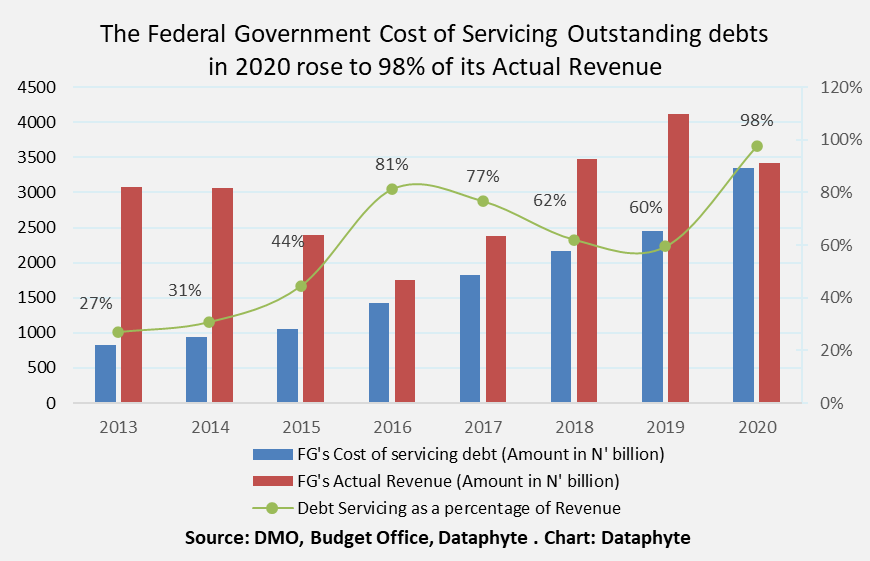

Nigeria currently services debts with almost all its annual revenue. While many policy experts warn that this is unsustainable, the Government is not relenting in its mission to run the country bankrupt.

Budget deficits arise when the government intends to spend more than its expected revenue in a year or given period. This situation usually warrants the government to opt for debts locally and internationally.

Then there is Nigeria’s other intractable deficit – the housing deficit. Nigeria has one of the lowest homeownership rates in the world, especially in its urban areas. In the urban centres, homeownership was as low as 35.7% by 2019, while the housing deficit across the country has soared to 25 million as of 2019, doubling the housing gap as of 2010.

Besides the need to build at least 25 million more houses, about 53 percent of the old housing stock or about 5 million houses will need to be reconstructed altogether. Another 32 percent of existing housing stocks need significant improvement, according to the ERGP estimates.

The Real Dilemma: Reducing one big Deficit Increases the other Deficit

Like a Siamese twin, efforts to make one life whole often bring the life of the other into great peril. The government’s efforts to reduce housing deficits, as with other gaps in public infrastructure, involve huge government spendings, which may attract more loan funding and increase budget deficits.

In all, Nigeria will need an annual investment of N35 trillion over the next six years to position its housing sector if information from the government’s own plans is to be taken, Dataphyte’s Housing Advisory noted.

The Federal Government’s Public Expenditure on the Provision of Housing

| 2018 | 2019 | 2020 | |

| Budgetary Allocation for Provision of Housing (N’ billion) | 68.57 | 54.02 | 41.84 |

| Actual Spending on the Provision of Housing (N’ billion) | 42.67 | 16.02 | N/A |

| Budget Performance (%) | 62.23% | 29.66% | N/A |

Source: OAGF

However, government budgets for the provision of housing do not measure up with the degree of spendings required to bridge the gap in Nigeria’s housing infrastructure. The housing budget declined from N68.57 billion in 2018 to N41.84 billion in 2020.

Moreso, only 62.23% of that budget was eventually spent in 2018. It was worse in 2019 when only N16.02 billion (amounting to 29.66%) of the N54.02 billion was eventually spent.

Government finance of housing was this meagre in 2019 in spite of the huge Government borrowing that year, estimated at N3 trillion, and crippling debts that had piled up to N27.4 trillion in the same year.

Thus, to expect the government’s sole investment in Housing to the tune of N35 trillion over the next 6 years is to induce a debt-driven policy suicide.

Yet to reduce or stall the government’s spendings on housing, in the bid to reduce debts and budget deficits will also amount to increasing housing deficit.

Besides, to halt the needed investment in the housing sector is to further discount an already declining contribution of the Real Estate sector to the overall output of the country.

Dataphyte’s housing advisory note suggests that, in view of the tight fiscal condition and the inability of the government at the national and sub-national level to borrow massively, economic planners may have to turn to the housing sector.

Furthermore, demand for homes can be stimulated by consumer credit (mortgage) to boost construction activities.

Clearly, with Nigeria’s housing deficit estimated to be in the region of 25 million housing, and the majority of urban dwellers residing in slums, the sector holds significant promise if government homes turn the corner, boost construction activities, create millions of jobs and upend the cycle of poverty, the Dataphyte advisory submitted.

The Real GDP of the Housing Sector: How Real is Real Estate?

For Real! Real estate development collocates with real economic growth. That is, the level of productivity in the Housing Sector of a country is strongly linked with its level of Economic growth. Dataphyte’s analysis of 14 years of historical data shows that there’s a 65% correlation between growth in housing output and growth in Nigeria’s Gross Domestic Product (GDP).

While such a positive and relatively strong relationship between housing and economic growth exists, it has not been universally established whether it is the performance of the housing sector that stimulates economic growth or it is the performance of the general economy that actually determines the outcomes in the housing sector.

There is still a debate as to the direction of causality. The central issue remains whether housing leads, follows, or complements economic growth and development, Uwatt (2019) observed.

The trend analysis also reveals that Real Estate growth movements were more elastic compared to the overall GDP growth movement. A sharp drop of 18.84 points in Housing GDP growth from 11.98% in 2013 to -6.86% in 2016 either responded to or caused a less steep drop of 7.07 points from 5.49% to -1.58% within the same period.

Besides, the general economy recovered from the negative growth of the 2016 recession faster than the real estate sector. On the other hand, the housing sector made a surprise comeback in 2020 from the COVID-19 induced recession.

Dataphyte analysts observe that the three possible relationships between housing and economic growth may be valid and that the direction of causality may vary in different economic and policy environments.

However, there is recent evidence from China that the performance of the housing sector causes significant changes in the general performance of the economy. The country’s recent policy to slow down investment in residential housing is immediately resulting in a decline in its overall GDP growth, Aljazeera reported.

Thus, Uwatt reiterates the view of many development economists that “housing is a part, rather than a by-product, of the economic development process and it contributes to growth. Therefore, adequate attention should be given to housing and its associated services, as they can contribute substantially to economic development.”

To Owe and to Own: Can the Mortgage Market mediate poverty and prosperity?

An Empirical Yes! Affordable mortgage products can make poor people less poor and more prosperous. Even more, it can stabilize a poor ostentatious and revenue-deficient government living on a debt-support machine.

First, deepening the mortgage market as well as housing bonds in the capital market results in a greater capital pool for housing finance, various studies have shown.

Housing finance differentiates the general interest rates from that for housing. It is meant to reduce the interest rate on loans for real estate, thereby decreasing the prices of houses and increasing the affordability of housing.

Linkages between Housing Finance and Economic Development

Diagram: Uwatt B. Uwatt, Housing Sector, Economic Growth and Development: Conceptual Issues and Theoretical Underpinnings, in Central Bank of Nigeria (2019)

Developing the mortgage markets results in cheaper mortgage plans for the poor, which relieves them from the burden of paying exorbitant and perpetual rents which impoverishes them the more.

Homeownership also increases the chances of the poor getting education. Studies cited in a World Bank Review Summary on Housing Finance and Poverty Reduction suggested that ““having a house as an asset improves homeowners’ borrowing capacity” and so housing finance could lead to more investment in human capital.

And to the extent that housing finance improves housing affordability for the poor, it may improve the probability of education opportunities for the poor.”

Also citing Jacoby & Skoufias (1997), the Housing Finance and Poverty Review reported that “without access to finance, shocks to income cause poor families to discontinue schooling for children. Housing provides an asset that can be used to smooth such shocks and thereby reduce the vulnerability among the poor.”

Besides these, Housing Finance significantly degrades unemployment levels, unemployment being a major cause of poverty.

The Dataphyte Housing Advisory notes that 1 job in the construction sector has the potential of creating 3 additional jobs in the economy.

Housing Finance and its Employment Potentials

| Housing Activity | Housing Employment Outcomes | Housing-induced Employment Outcomes | |

| USA | 100 new low-income housing being built | 80 jobs from the direct and indirect effects of construction | 42 jobs from induced effects of increased spending |

| Argentina | 1 million pesos investment in housing construction | 40 direct jobs 20 indirect jobs | Unestimated number of jobs created further in the backward and forward linkages |

| India | 1 million dollars investment in building construction | 600 direct jobs 1000 indirect jobs | Unestimated number of jobs created further in the backward and forward linkages |

Source: World Bank Review – Housing Finance and Poverty Reduction

Besides, the Construction sector has potential to provide employment for those with little education or skill, many of them from the very low-income sections of society. Recent surveys of construction workers in a number of Nigerian cities have revealed that they are predominantly young and uneducated (Abdul, 2020). This also further reduces income inequality.

Budget Deficits & Housing Deficits: Can the 2 Deficiencies be treated with 1 Supplement?

Sure guess! The development of the mortgage and capital markets! This could deliver the quantum of capital to finance Nigeria’s housing deficits.

And while at it, private capital relieves the government of the burden of borrowing costly funds to spend on residential housing in order to catch up with the shortfall.

Housing construction, financed at a lower cost of capital from the mortgage and capital markets, also yields needed tax revenue to the government. This includes “construction related taxes, sales taxes on building materials, corporate taxes on builders’ profits, income taxes on construction workers, and fees for zoning, inspections, etc.”

Thus, while dealing with the housing deficit with mortgage-financed housing investments, housing activities are also dealing with the government’s budget deficits through reduced debts and increased revenues from housing-related taxes.

And in all, the people benefit from increased access to affordable housing and other public infrastructure that a more financially-stable government can provide.