In April 2022, Nigeria’s President, Muhammadu Buhari, said that his government had done much to create an enabling environment for micro-, small- and medium-scale enterprises (MSMEs) to thrive.

He said this to emphasise the importance of MSMEs to the country’s economy.

In this report, Dataphyte looks at how easy or difficult it is for MSMEs to access loans from banks.

READ ALSO: CBN cash withdrawal policy threatens to reverse POS successes

What Data say about SMEs in Nigeria

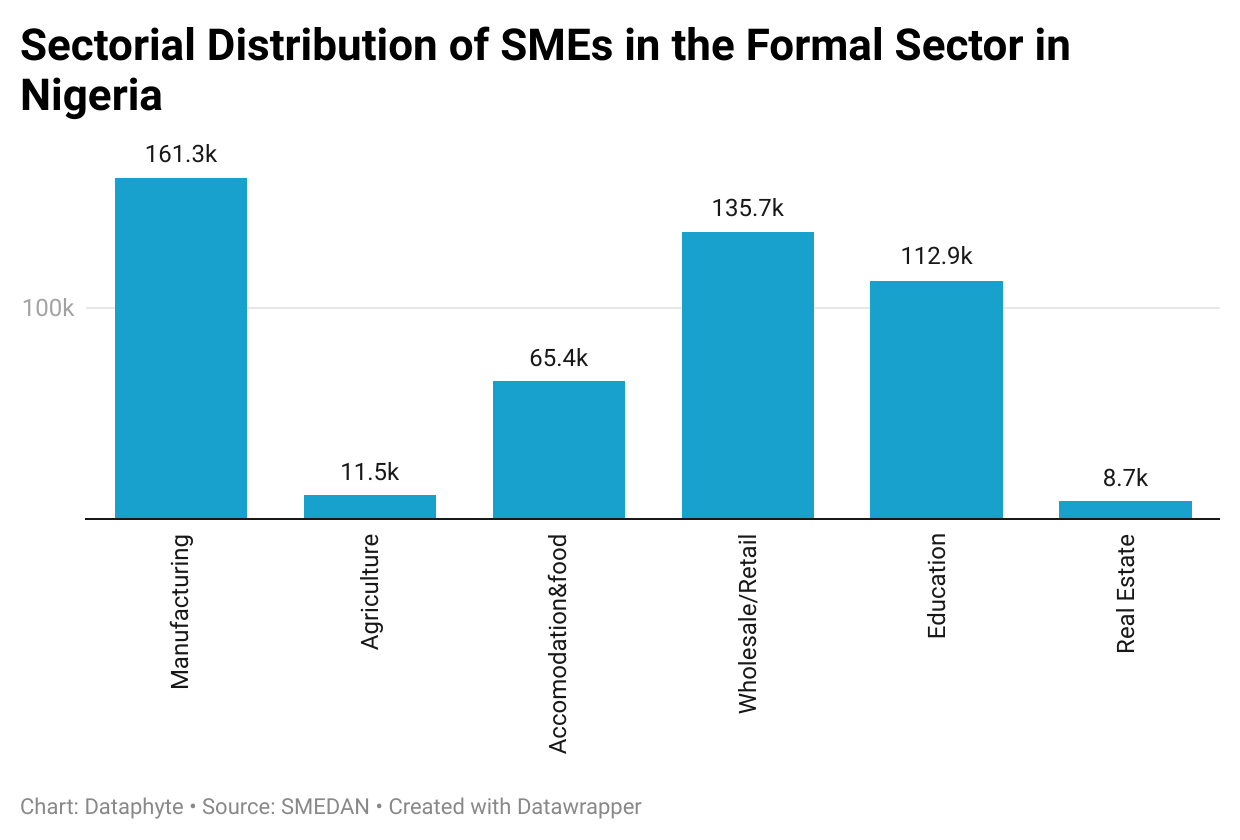

In a recent survey published by the Small and Medium Enterprises Development Agency (SMEDAN) and the National Bureau of Statistics (NBS), the number of MSMEs in the country dropped from 41.169 million recorded in 2017 to 38.413 million in 2020. This means that 2.756 million enterprises closed operations within the three-year period.

These organisations cut across different sectors of the country, from manufacturing to mining and quarry, education, information and communications, and agriculture, among others.

The survey also shows that there are 617,248 small-scale enterprises and 53,199 medium-scale enterprises that are in the formal business sector of the country.

MSMEs are responsible for 51.74 million jobs in the country, according to the SMEDAN/NBS survey.

The 2017 data on MSMEs showed that MSMEs contributed 49.78 percent to Nigeria’s GDP at that time.

The SMEDAN’s 2020 survey has revealed that a significant challenge faced by MSMEs is financing.

MSMEs face cash crunch

A review of financial statements published by the Guaranty Trust Bank has shown that MSMEs got 3.3 percent of the total loans and advances issued by the bank between 2021 and June 2022.

Documents published by the bank showed that as of June 2022, the financial institution released a total sum of N1.533 billion as loans and advances.

However, SMEs accounted for N24.8 million, representing 1.6 percent of the total.

In 2021, a total sum of N1.475 billion was disbursed as loans and advances, with SMEs receiving the sum of N25.5 million, representing 1.7 percent of the entire loan paid out.

Between 2021 and June 2022, a total sum of N3.008 billion was devoted to loans and advances.

A review of the financial statement of Zenith Bank also reveals the pattern of loans and advances granted to MSMEs.

In the 2021 financial year, MSMEs and commercials got 18.7 percent of the loans and advances. The total loans disbursed in the period stood at N3.50 trillion. This would mean that the sum of N654.5 million was approved as loans and advances by the bank for the financial year.

In 2022, the bank disbursed 19.1 percent of its loans and advances to SMEs and commercials.

Zenith Bank’s total loan paid as of Q3 2022 stood at N4.06 trillion, meaning the sum of N775.46 million was received by SMEs and commercials.

The Borgen Project notes that inadequate collateral is a major reason MSMEs fail to receive loans from banks in the country.

The PricewaterhouseCoopers (PWC) also revealed in its report that the financing gap for SMEs in the country stood at N617.3 billion annually.

It has been reported that 80 percent of MSMEs in the country fail in the first five years of formation.

This concern made the Central Bank of Nigeria start the Agri-business, Small and Medium Enterprises Investment Scheme in 2017. The programme supports government efforts for MSMEs as vehicles for economic development and employment generation.

The scheme mandates banks to set aside 5 percent of their profit after tax annually to contribute to the fund.

This is apart from other funds which the government is investing in MSMEs.

Despite these efforts, reports have noted that MSMEs still need help accessing loans, with the Credit Bureau Association of Nigeria noting that only 4 percent of small businessses have access to credit in the country, despite efforts of the country through different policies.

SMEDAN offers hope

A SMEDAN official, Tana Abdul, told Dataphyte that the organisation had been making substantial efforts to support MSMEs’ access to finance.

“The major problem MSMEs face is that of the interest rates of banks, which are unfavourable to them. Also, sometimes, banks prefer to grant loans to corporate organisations that can pay larger interest rates than to SMEs that cannot afford to pay the rate they set.”

She also identified a problem with the banks’ ranking of MSMEs’ capacity to pay back loans.

The SMEDAN staff member, however, noted that there were substantial efforts by the government agency to help SMEs smoothen the process, although that was minute, given the number of MSMEs in the country.

Experts have consistently said that banks prefer to lend to large enterprises as they consider most MSMEs as high-risk. But they caution that doing so would not help the Nigerian economy to achieve high growth rates.

“Banks’ interest rates are so high, but large enterprises get them at low rates. Even the so-called intervention funds of the CBN are not easily accessible to MSMEs. These things have refused to change,” said former Chairman of SME Group of the Lagos Chamber of Commerce and Industry, Jon Kachikwu.

Nigeria must invest in MSMEs to create jobs

A policy expert, Samuel Atiku, told Dataphyte that there was a need for the government to prioritise MSMEs development in the country..

“We should address growing concerns of these MSMEs, startups and make them see reasons to continue doing business. Doing that will enable us to create millions of jobs and boost the economy. It is not rocket science; it is just what will be obtainable. We need to invest in our MSMEs sector like other countries do and even train them,” Atiku added.

Get real time update about this post categories directly on your device, subscribe now.

{kind=link}